The type of account defines whether a transaction either debits or credits that account. With single-entry bookkeeping, online bookkeeping you enter each transaction only once. If a customer pays you a sum, you enter that sum in your asset column only.

We’ll do one month of your bookkeeping and prepare a set of financial statements for you to keep. Accounting is a high-level process that uses financial information compiled by a bookkeeper or business owner, and produces financial models using that information. One of the most essential tasks a bookkeeper will do for a small business is making sure they don’t run out of day-to-day money.

Double entry is an accounting term stating that every financial transaction has equal and opposite effects in at least two different accounts. A trial balance is a worksheet with two columns, one for debits and one for credits, that ensures a company’s bookkeeping is mathematically correct. An accountant typically has a degree and relevant work experience, however, there is no formal certification process for becoming an accountant. Taking a few accounting courses and developing a basic understanding of accounting will qualify you for a job in bookkeeping. To work in accounting, you must have at least a bachelor’s degree to become an accountant or, for a higher level of expertise, you can become a certified public accountant.

Entry Systems

Whether you’ve worked as a small-scale accountant or as a company’s controller, that experience will go a long way in landing clients for your own business. The total amount of debits must equal the total amount of credits in a transaction.

A large aspect of accounting is presenting the information in the form of general-purpose financial statements, such as a balance sheet or income statement. T Account – T accounts are a useful bookkeeping tool used to visualize double entry bookkeeping journal entries before they are posted.

The double entry system provides for checks and balances by recording a corresponding credit entry for each debit entry. Single entry bookkeeping system is a basic system that a company might use to record daily receipts or generate a daily or weekly report of cash flow. The single entry system of bookkeeping requires recording one entry for each financial activity or transaction. Absolute recording of transactions– It is concerned with a complete and permanent record of all transactions in a systematic and logical manner to show its financial effect on the business.

For example, you may find yourself in a dispute with a vendor or under audit by the government. Without clean financial records, you may be at risk of paying settlements or tax penalties for avoidable financial errors.

In some small businesses, the bookkeeping and accounting functions are both outsourced. If you outsource your bookkeeping and accounting, you’ll still want to be familiar with them both to understand the reports you’ll receive. Cash-based accounting is what is the difference between bookkeeping and accounting much simpler than accrual basis accounting. In cash-based accounting, you record revenue when you receive it, and record payments when they are made. This method is usually limited to small businesses in the service industry that has no inventory.

The other tab is for CPA and Bookkeepers to learn how to manage their client’s accounts. The Balance Sheet, the Statement of Cashflows, and the ___ are three key financial statements.

While some individuals may benefit from a QuickBooks certification, others may find it unnecessary. While you cannot claim to be “certified” with QuickBooks without the certification process, that doesn’t stop you from otherwise becoming proficient in—or even mastering—the bookkeeping software. While you should always learn how to use your chosen accounting software correctly, you don’t require a personal certification to do so. A company’s transactions are recorded in a general ledger and later summed to be included in a trial balance.

What are the two types of bookkeeping?

Types of Bookkeeping system. The single-entry and double-entry bookkeeping systems are the two methods commonly used. While each has its own advantage and disadvantage, the business has to choose the one which is most suitable for their business.

The purpose of the balance sheet is to provide an idea of a company’s financial position. It does so by outlining the total assets that a company owns and any amounts that it owes to lenders or banks, for example, as well as the amount of equity. Trial Balance is a simple listing of Nominal Accounts with Debit Balances posted into Debit and Credit Balances posted into Credit Columns. It ensures that for every debit amount, there is an equal credit amount and vice versa.

- The chart of accounts usually includes balance sheet accounts and income statement accounts, according to the AccountingCoach.com.

- Balance sheet accounts are assets, liabilities, and stockholder or owner equity.

- Income statement accounts are operating and nonoperating revenues, expenses, gains and losses.

Cash Flow Statement

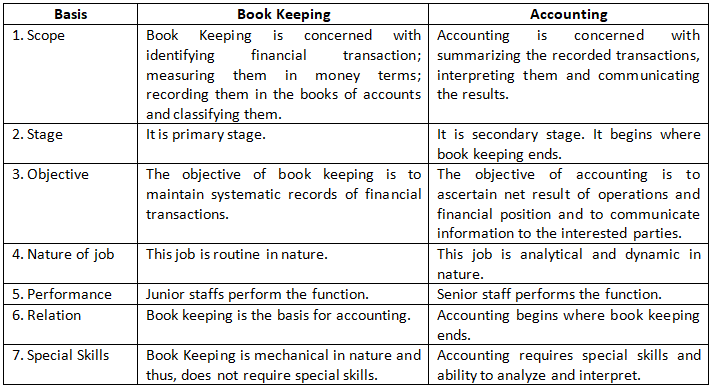

While bookkeeping and accounting are very similar in their functions, there are significant differences between these two roles. This article discusses 5 major distinguishing factors between bookkeeping and accounting, and how each position plays an important part in business growth and sustainability.

For larger limited companies, a balance sheet must be filed once a year as part of the company’s statutory accounts. In Balance Method, all ledger accounts are balanced and these balances are taken for the preparation of Trial Balance. Bookkeepers handle the recording aspect of all accounting processes, accountants handle all parts of the accounting process. It can process accounts faster, increase reporting accuracy, and your data is backed up. Bookkeeping is the recording, storing, and retrieving of financial transactions for an individual, company, or nonprofit organization.

Developing a more robust set of offerings is also a solid way to attract new clients. Since you’re dealing with someone else’s private and sensitive data as a bookkeeper, you should also get insurance to protect yourself and your company should mistakes or catastrophe happen.

What An Accountant Does

Software changes over time, and your certification will only certify you for one version of QuickBooks. Consider re-certifying every year or several years to keep bookkeeping your QuickBooks certification current. You can also take classes on QuickBooks basics through a variety of accredited colleges or other educational institutions.

Plus, most accounting software starts you off with double-entry bookkeeping anyway. With the software all ready to go, you can tackle double-entry bookkeeping with no sweat.

Have Experience Or Learn Bookkeeping.

What is simple bookkeeping?

Bookkeeping is the process of recording company’s daily financial transactions. Proper bookkeeping enables companies to track all financial data. It also enables them to make correct financial decisions on time. Through proper bookkeeping companies can measure their financial performance as well. Types Of Bookkeeping.

Accounting Records – The records of all the transactions of the business. Many bookkeeping and accounting offices are willing to let high school or college students work part-time as interns. They get help with their jobs, and you get a first-hand look at what it’s like to work as a bookkeeper. Maintain up to date certification by going through the certification process several times through your career.

A big question is whether bookkeepers are as regulated as accountants. As we know, there are numerous types of certifications for accountants around the world, primarily Certified Public Accountants (CPAs) and Chartered Accountants (CAs). And you aren’t an ‘official’ accountant without one of those designations, and they take many years of study and many thousands of dollars to attain. Accounting is a system for measuring, processing and communicating financial information.

Balance Sheet – What Is A Balance Sheet?

It’s a bookkeeper’s job to make sure that the accounts are valid and up-to-date when the accountant needs them. http://www.hotelwangu.com/?p=69413 This lets an accountant use their knowledge to make business recommendations and complete any tax returns.